As the tax season approaches and property valuation updates roll out across Malaysia, homeowners, real estate investors, and B2B commercial operators in Johor find themselves facing the same recurrent challenge. When calculating assets, filing tax returns with the Lembaga Hasil Dalam Negeri (LHDN), or drafting tenancy agreements for a new commercial space in Johor Bahru, a fundamental legal and financial question arises: what exactly separates a piece of furniture from a property fixture? While the terms are often used interchangeably in casual conversation, the legal and financial boundaries between them are distinct, carrying significant consequences for your wallet.

For a business operating a bustling B2B office in the heart of Iskandar Puteri, misclassifying these assets can lead to lost opportunities for claiming capital allowances. For a residential landlord leasing out a high-rise condominium in Mount Austin, failing to clearly define these terms in a tenancy agreement can result in expensive legal disputes over what a tenant is legally permitted to dismantle and take with them when the lease expires. Understanding the structural, legal, and tax-based difference between furniture and fixtures is not merely an academic exercise—it is an essential operational requirement in 2026.

The Legal Framework: Degrees and Purposes of Annexation

In Malaysian property law, which draws heavily from English Common Law principles, distinguishing between a chattel (movable personal property, i.e., furniture) and a fixture (immovable property attached to the land) is governed by two main tests. These are the “Degree of Annexation” test and the “Purpose of Annexation” test. Real estate appraisers and legal courts in Johor consistently apply these tests to settle disputes between buyers and sellers, as well as landlords and tenants.

The **Degree of Annexation** test analyzes the physical attachment of the item to the property structure. If an item is secured to the floor, walls, or ceiling using nails, bolts, cement, or heavy industrial adhesives, there is a legal presumption that it has become a fixture. The core question is: can this item be removed without causing structural damage to the surrounding property? For instance, a free-standing, modular wooden wardrobe sitting in a bedroom is held in place entirely by gravity. It can be easily carried out of the house without altering the walls. This is furniture. On the other hand, custom built-in floor-to-ceiling wardrobes that are physically anchored to the concrete wall panels are considered fixtures. Removing them would tear away plaster, damage the underlying drywall, and leave exposed structural cavities.

However, the physical connection is not the only factor. The court must also apply the **Purpose of Annexation** test, which often takes precedence over the physical connection. This test examines the intention behind placing the item in the property. Was the item attached to the building to make the building itself more functional and habitable as a permanent structure, or was it attached simply to enhance the enjoyment of the item itself? A classic example is a wall-mounted air conditioning unit—a vital feature for any home or office in Malaysia’s tropical heat. Even though the interior compressor unit is hung on brackets and can be detached with relative ease, the system is installed to make the building habitable for living and working. Therefore, air conditioning systems are legally classified as fixtures. Conversely, a large, heavy oil painting hung from a heavy-duty wall anchor is physically secured to the wall, but the purpose of that attachment is simply to display the artwork for personal enjoyment. It does not improve the permanent utility of the building, meaning it remains classified as furniture (or personal chattel).

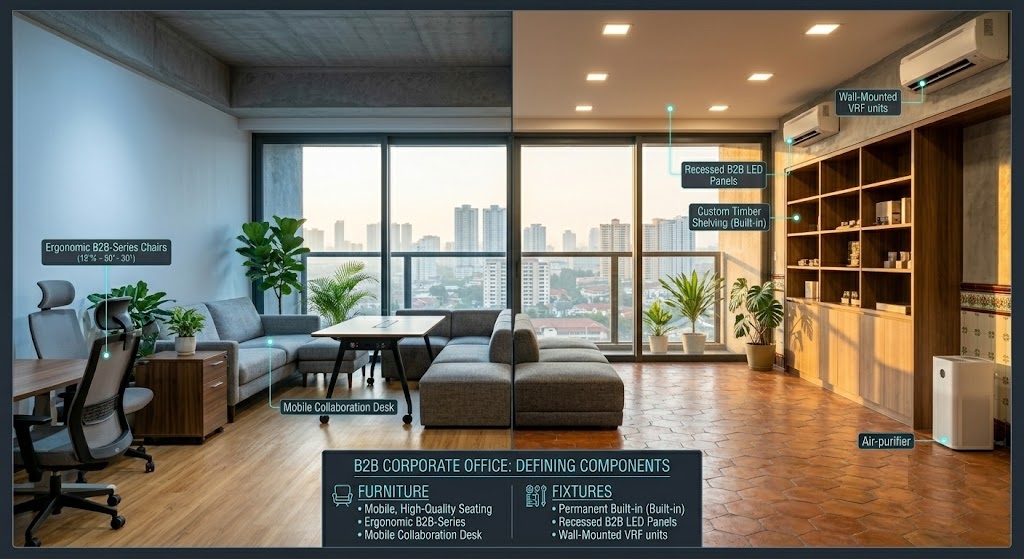

Tax Implications: LHDN Capital Allowances for B2B Offices

For businesses operating in Johor’s rapidly expanding commercial zones, such as Medini or Johor Bahru City Centre, understanding the distinction between furniture and fixtures is vital during tax season. Under the Malaysian Income Tax Act 1967, business entities can claim tax relief on the depreciation of business assets through **Capital Allowances (CA)**, rather than deducting the depreciation directly from their profit and loss accounts. However, to claim these allowances, assets must be accurately categorized according to LHDN’s strict guidelines [1].

Under LHDN Public Rulings, business assets are broadly divided into “Plant and Machinery,” which are eligible for capital allowances, and structural buildings, which are not [1]. Within a typical corporate office fit-out, the lines can blur. Items classified as “furniture and fittings” (such as office desks, ergonomic task chairs, free-standing partitions, and mobile filing cabinets) qualify for a standard Initial Allowance of 20% and an Annual Allowance of 10% [1]. This means the entire capital expenditure on these loose items can be fully written off against tax within four years [1].

Fixtures, however, present a more complex scenario. If a business spends RM 100,000 installing custom built-in gypsum board partitions, false ceilings, and integrated recess lighting to design their workspace, they must evaluate whether these additions qualify as “plant” (functional tools for the business) or simply as part of the building structure itself. LHDN guidelines state that while general lighting fixtures and basic electrical wiring do not qualify for capital allowances because they are considered part of the building’s basic infrastructure, specialized electrical installations, custom server room cooling systems, and dedicated backup power supplies *do* qualify as plant [1]. Misallocating these expenditures on tax returns can result in severe audit penalties, audit delays, or missed tax deductions, impacting a business’s cash flow during challenging economic cycles.

When preparing tax filings for a business in Malaysia, always maintain a detailed Asset Register that separates movable furniture from built-in structural fittings [1]. LHDN auditors frequently scrutinize renovation and refurbishment accounts. If your general ledger combines custom built-in partition walls (non-qualifying structure) with loose workstation furniture (qualifying fittings) under a single “Renovation” entry, the entire claim may be disallowed during an audit [1].

The Tenancy Angle: Protecting Landlords and Tenants in Johor

The residential and commercial leasing market in Johor is highly active, with many Singaporean expats and local professionals moving into modern developments. In these high-stakes rental markets, misunderstandings regarding furniture versus fixtures are among the most common sources of conflict between landlords and tenants when a lease terminates.

Under a standard Malaysian tenancy agreement, there is an implied legal understanding that at the end of the tenancy, the tenant must hand the property back to the landlord in its original condition, minus reasonable wear and tear. This means that any “fixtures” added by the tenant during their lease—such as built-in custom kitchen cabinets, designer light fixtures, or luxury bathroom vanity units—automatically become the property of the landlord and cannot be removed without prior written consent. If a tenant attempts to dismantle these built-in elements upon moving out, they are legally liable for property damage and breach of contract.

However, loose “furniture” added by the tenant—such as dining tables, sofa sets, free-standing bed frames, and televisions—remains the exclusive personal property of the tenant. They are fully entitled to pack up these items and transport them to their next home. The conflict arises when items exist in a legal grey area, such as custom-mounted flat-screen television brackets, window blinds, or smart home security cameras. To prevent these disputes from escalating to the Johor Bahru Small Claims Tribunal, landlords must include a detailed, itemized inventory list in the tenancy agreement. This document should explicitly state which items are classified as landlord fixtures, which are provided as loose landlord furniture, and what the tenant is legally permitted to modify or remove at the end of their stay.

Property Valuation: How Fixtures vs. Furniture Impact Real Estate Appraisals in Johor

For property owners, real estate investors, and developers across Johor, property valuation is a crucial financial mechanism. Whether you are dealing with a luxury residential high-rise in Puteri Harbour or a light industrial warehouse in Pasir Gudang, understanding how bank appraisers treat furniture versus fixtures is critical. When a licensed valuer conducts an inspection of a property for a mortgage application or refinancing evaluation, they analyze the physical space through a highly conservative legal and financial lens.

To a bank valuer, “fixtures” are considered an integral, permanent part of the real estate asset. Because these items are legally annexed to the land and building structure, they are included in the overall valuation of the property. This means that high-quality, permanent installations—such as custom-designed wet and dry kitchens, built-in plaster ceilings with integrated lighting, premium bathroom sanitary ware, and structural flooring upgrades—directly contribute to pushing up the property’s appraised value. If you spend RM 50,000 on a built-in kitchen cabinet system that is seamlessly integrated into the property’s masonry, that expenditure is recognized as a capital improvement that enhances the value of the property for mortgage purposes.

Conversely, “furniture” is completely disregarded during a standard real estate valuation. A homeowner might invest RM 100,000 in importing luxury Italian leather sofas, free-standing solid teak wood dining tables, and designer bedroom sets. Yet, when the bank’s valuer calculates the market value of the property to approve a buyer’s home loan, they will value all of that loose furniture at exactly RM 0. The reason is simple: loose furniture is highly liquid, movable, and personal. Since the owner can easily load these items onto a truck and drive away, they do not form part of the bank’s underlying collateral. If a property goes into foreclosure, the bank can only repossess the land and the permanent structures—not the loose furniture. Therefore, relying on expensive loose furniture to inflate the appraisal value of a property is a critical mistake.

Custom Built-ins vs. Loose Furniture: The Financial Trade-off

For modern homeowners and office managers in Johor Bahru, furnishing a space always involves a strategic balancing act between custom-built fixtures and loose, modular furniture. Each path has distinct financial, functional, and long-term consequences that must be carefully evaluated before signing a contractor agreement.

Custom built-in fixtures offer the distinct advantage of spatial optimization. In urban high-rises where square footage is at a premium, custom built-in wardrobes can maximize vertical space, utilizing awkward corners and sloping ceilings that standard furniture cannot accommodate. They create a seamless, integrated aesthetic that often feels highly luxurious and permanent. However, the financial trade-off is significant. Custom built-ins require high upfront material and labor costs, and they are completely illiquid. If you decide to sell your home or relocate your business to a new commercial hub, you cannot take these built-ins with you. They must be abandoned, and as established, you will only recover a fraction of their cost through property appraisal, if at all.

On the other hand, loose modular furniture offers unmatched financial and operational flexibility. If a B2B business in Johor decides to scale down its physical office footprint in favor of a hybrid work model, loose furniture remains a tangible asset that can be easily sold, relocated to a smaller branch, or stored. It represents a flexible asset that does not bind your capital to a single geographic location. Furthermore, because loose furniture is manufactured in controlled factory environments, it is often far more cost-effective than hiring carpentry contractors to build custom fixtures on-site, where mistakes and delays can quickly inflate budgets. By prioritizing high-quality loose furniture over custom built-ins, property owners retain control over their capital, ensuring that their interior design investments remain adaptable to future life changes or business restructuring.

| Analytical Metric | Movable Furniture (Chattels) | Permanently Attached Fixtures |

|---|---|---|

| Physical Attachment | None. Sits under its own weight; easily moved by hand or dolly. | High. Bolted, screwed, cemented, or wired into the structure. |

| LHDN Tax Treatment | Qualifies as Furniture & Fittings (20% Initial, 10% Annual Allowance). | Specialized fixtures qualify as Plant; structural fixtures do not. |

| Property Valuation Impact | Valued at RM 0 by banks; excluded from mortgage appraisals. | Directly increases property value; included in bank appraisals. |

| Lease Expiry Ownership | Remains the property of the tenant; must be removed upon moving. | Becomes the property of the landlord; cannot be removed. |

| Removal Damage | Zero structural damage to walls, ceilings, or floors. | Requires demolition, patching, plastering, and repainting. |

| Examples | Sofas, loose desks, armchairs, stand-alone cabinets, TVs. | Built-in kitchens, central air ducts, toilets, partition walls. |

The B2B Office Shift: Why Flexible Modular Furniture is Overtaking Built-In Fixtures

In the wake of shifting economic landscapes and corporate restructuring in 2026, commercial tenants in Johor’s main commercial zones, such as Mount Austin, Taman Molek, and Medini, are fundamentally changing how they design their workspaces. The era of the heavily built-out corporate headquarters—filled with permanent plasterboard partition walls, custom built-in reception counters, and rigid built-in executive suites—is rapidly coming to an end. Today’s businesses are prioritizing agility, and this preference is reflected in the massive shift from permanent fixtures to loose, flexible modular furniture systems.

The primary driver behind this transition is the harsh reality of commercial tenancy handovers. In Malaysia, commercial leases typically require the tenant to restore the office space to its original “bare shell” condition when the lease terminates. If a business has spent hundreds of thousands of ringgit installing built-in fixtures, they must spend even more money at the end of the tenancy to hire demolition contractors to tear those fixtures down, patch the concrete floors, and repaint the walls. This double expenditure is a massive financial drain that yields zero return on investment.

By opting for flexible, modular furniture systems—such as height-adjustable desks, mobile acoustic screens, modular conference tables, and loose lounge seating—companies can design a highly functional, beautiful office space that can be packed up and moved in a single weekend. If the business grows, they can easily reconfigure the modular furniture to accommodate more workstations. If the business decides to relocate to a more modern office tower, the entire furniture setup moves with them, preserving their capital investment. Furthermore, as we explored in the tax section, loose office furniture and fittings are highly tax-efficient, allowing businesses to write off their costs quickly under LHDN’s Schedule 3 capital allowances, whereas permanent structural partitions offer little to no tax relief.

Practical Checklist for Malaysian Home Buyers, Landlords, and B2B Office Managers

To protect your investments, minimize your tax liabilities, and avoid legal disputes, it is essential to establish a standardized, systematic approach to managing your property assets. Whether you are buying a new home, managing a commercial lease, or preparing for tax season, use this practical checklist to ensure absolute clarity between furniture and fixtures:

1. Review the Sale and Purchase Agreement (SPA) Carefully

When purchasing a sub-sale residential property or commercial lot in Johor, never assume that the items you saw during your viewing are included in the purchase price. The SPA must include a highly detailed “Inventory of Chattels and Fixtures” annexure. This list must explicitly state which items are included in the sale (such as air conditioners, kitchen hoods, or built-in wardrobes) and which items the seller is legally required to remove before key handover. Clear documentation prevents frustrating disputes on moving day.

2. Maintain a Split Asset Register for LHDN Compliance

For B2B business operations, work closely with your accounting team or corporate tax agent to ensure that all renovation invoices are itemized. Do not accept a lump-sum “renovation” invoice from your fit-out contractor. Insist on a detailed breakdown that separates structural alterations (fixtures) from loose workspace furniture (furniture and fittings). This clear separation is crucial for maximizing your Capital Allowance claims under LHDN guidelines and surviving a potential tax audit.

3. Implement Detailed Inventory Lists in Tenancy Agreements

If you are a landlord leasing out a semi-furnished or fully furnished property in Johor Bahru, protect your assets by attaching a comprehensive, photographic inventory list to your tenancy agreement. Each item should be clearly classified as either a fixture (which the tenant cannot touch) or a piece of furniture (which the tenant must maintain and return in good condition). Specify the financial penalties for unauthorized removal or damage to any item on the list.

Conclusion: Mastering the Asset Divide

The distinction between furniture and fixtures is far more than a minor detail in interior design. It is a critical boundary that impacts tax liabilities, bank appraisals, commercial lease negotiations, and long-term investment strategies. For homeowners, understanding this divide prevents costly mistakes during property sales and ensures that renovation budgets are allocated to projects that actually enhance the property’s bank valuation. For businesses, mastering this classification is the key to maintaining financial agility, maximizing tax deductions under LHDN capital allowances, and avoiding expensive reinstatement costs at the end of a commercial lease.

As the Malaysian property and commercial landscapes continue to evolve in 2026, the demand for flexible, high-quality, and tax-efficient loose furniture has never been higher. By prioritizing modular, loose furniture over permanent custom built-ins, you maintain control of your capital, protect your peace of mind, and ensure your space remains adaptable to whatever the future holds.

If you are looking to design a dynamic, highly adaptable office environment or elevate your residential space with premium, loose assets that support your lifestyle and financial goals, we are here to help. Skip the stress of permanent construction, avoid the complexities of fixture disputes, and discover the ultimate in flexible luxury. Visit our modern furniture shop today to browse our curated collections of premium desks, ergonomic seating, and modular home furnishings designed for the discerning Malaysian property owner.